監査の内容とは?

監査役監査の概要と目的

監査役監査とは、株主総会で選任された監査役が、取締役の職務執行について適法性・妥当性を評価する監査です。 取締役の職務執行が法令や定款などのコンプライアンスを遵守しているかを監査し、必要に応じて取締役に対する助言や勧告を行います。

キャッシュ

監査の目的は何ですか?

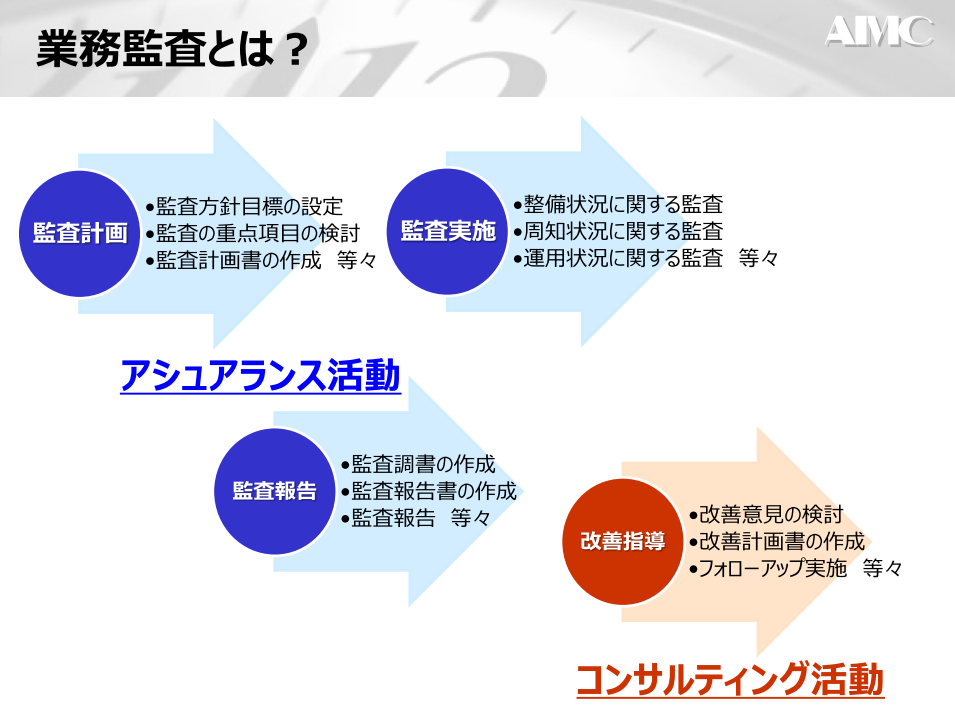

業務監査の目的 業務監査には、業務執行のプロセスでの法律やルールが遵守されているかを確認することと、経営目標の効果的な達成や業務改善を行う目的で行われます。 業務手順の整備状況と運用状況をチェックして報告するアシュアランスと、監査結果を受けて改善のための助言を行うコンサルティングの段階があります。

キャッシュ

監査の仕事とは?

「内部監査」は、社内のほか部署から独立した立場で、経営や業務に不正や誤りがないかをチェックします。 具体的には、経理部門を対象にした「会計監査」や、取締役の職務執行に不正がなく、法令・定款などを遵守して行われているかどうかを調べる「適法性監査」をしています。

監査部 何をする?

内部監査は、経営目標の達成に向けて適切な業務がなされているかを確認することが主な目的です。 他には財務状況や業務状況を調査・分析しながら、業務の効率化や不正を抑制し、調査結果を経営者に報告します。 一方、外部監査は顧客要求が守られているかを対外的に証明することが主な目的です。

キャッシュ

監査の手順は?

内部監査の手順監査計画を立てる予備調査を行う本調査を行う調査結果の評価・報告を行う監査手続き後の改善を行う

監査と査察の違いは何ですか?

監査と査察の大きな違いは、その目的が違うことである。 査察は、基本的に承認や許可のために確認する行為であり、査察官は、GMP省令等に違反する点がないかを調査し、審査する。 適合することにより、承認等が付与される。 監査は、契約や取り決めに反する行為がないかの確認である。

監査 いつやる?

監査法人の繁忙期は、主に上場会社の決算が終わった後の法定監査の時期です。 3月決算の企業を考えた場合、経理部が決算を締めるのが4月中旬までになり、その後に会計士による会計監査が始まります。 そして繁忙期としては、5月のゴールデンウィークが該当します。

監査の流れは?

企業監査の大まかな流れ

監査時には数人で編成された監査チームが組まれ、予備調査が実施されます。 予備調査時には、企業内部に監査に対応できる体制が整備されているかをチェックします。 ここで不備がなければ監査計画が立案され、監査がスタートします。 監査後は監査調書を作成して、外部の公認会計士が評価を行います。

監査業務の一覧は?

業務監査の流れ①予備調査の実施 本監査に先立ち、予備調査を行うのが一般的です。②監査計画の策定 予備調査の結果を基に、監査要点や実施に関する計画を作成します。③本監査の実施④評価~報告書作成⑤監査結果の報告⑥改善への助言と提案~再監査

内部監査は大変ですか?

内部監査の仕事はきついのか

他部署の社員との関係構築や業務遂行に関する悩みが多く挙げられています。 業務上、他部署と良好な関係を構築する必要がありますが、監査対象部署が協力的でない場合や、監査結果の指摘事項がスムーズに受け入れられない場合もあり、コミュニケーションにストレスを感じることもあります。

監査業務の流れは?

業務監査の流れ①予備調査の実施 本監査に先立ち、予備調査を行うのが一般的です。②監査計画の策定 予備調査の結果を基に、監査要点や実施に関する計画を作成します。③本監査の実施④評価~報告書作成⑤監査結果の報告⑥改善への助言と提案~再監査

監査手続の具体例は?

監査手続(かんさてつづき)

監査手続は、内部統制を把握した上で、試査によって実施されます。 具体的に監査手続には、実査、立会、視察、閲覧、確認、質問、証憑突合、計算突合、勘定分析、分析手続等があります。

査察が入るとはどういう意味ですか?

査察は、国税犯則取締法に基づく「強制」的な調査で、臨検、捜索、差押等の権限があり、悪質な脱税を摘発することが目的です。

監査は何人?

監査役は、株主総会において、監査役の報酬について意見を述べることができる。 大会社かつ公開会社では、監査役は3人以上であることを要し、かつ1人以上の常勤の監査役を定めなければならない。

内部監査 どこまで?

つまり、内部監査には、どこまでという概念がありません。 もちろん監査は自己監査となってはならないという原則がありますが、部門ごとに存在するインセンティブを考慮せず調査できる部門は内部監査室しかありません。 よって、内部監査室の業務範囲を広げることで、会社の利益を向上させる監査部門とすることができると考えられます。

業務監査の手順は?

業務監査の流れ①予備調査の実施 本監査に先立ち、予備調査を行うのが一般的です。②監査計画の策定 予備調査の結果を基に、監査要点や実施に関する計画を作成します。③本監査の実施④評価~報告書作成⑤監査結果の報告⑥改善への助言と提案~再監査

監査と会計監査の違いは何ですか?

監査役の行う監査には「業務監査」と「会計監査」があります。 「業務監査」とは、取締役の職務の執行が法令や定款に違反していないかに関し、行われる監査です。 「会計監査」とは会社の会計に関して行われる監査を指します。 それぞれ監査役の行う重要な業務であると言えるでしょう。

業務監査の内容とは?

業務監査 業務監査とは、会計業務以外の業務活動全般および組織・制度を対象とした監査です。 経営目標の達成に向けて合理的に業務が行われているか、法令や各種規定に沿って業務が遂行されているかなどを評価・報告することが目的です。

査察と監査の違いは何ですか?

監査と査察の大きな違いは、その目的が違うことである。 査察は、基本的に承認や許可のために確認する行為であり、査察官は、GMP省令等に違反する点がないかを調査し、審査する。 適合することにより、承認等が付与される。 監査は、契約や取り決めに反する行為がないかの確認である。

税務調査はなぜ来るのか?

法人税や所得税をはじめとする多くの税金は、納税者(法人、個人)が自ら税額を計算して申告・納付する「申告納税制度」が採用されています。 税額の計算ミスや虚偽の申告の可能性もあるため、不正行為の防止や申告内容の確認を目的に税務調査が行われています。