現金過不足の科目区分は?

まとめ 現金過不足は、実際の現金残高と会計ソフト上の残高が一致しないときに、一時的に使う勘定科目です。 決算時までに原因が判明しなかった場合には「雑収入」「雑損失」に振り替えて処理をします。

キャッシュ

現金過不足 仕訳 どっち?

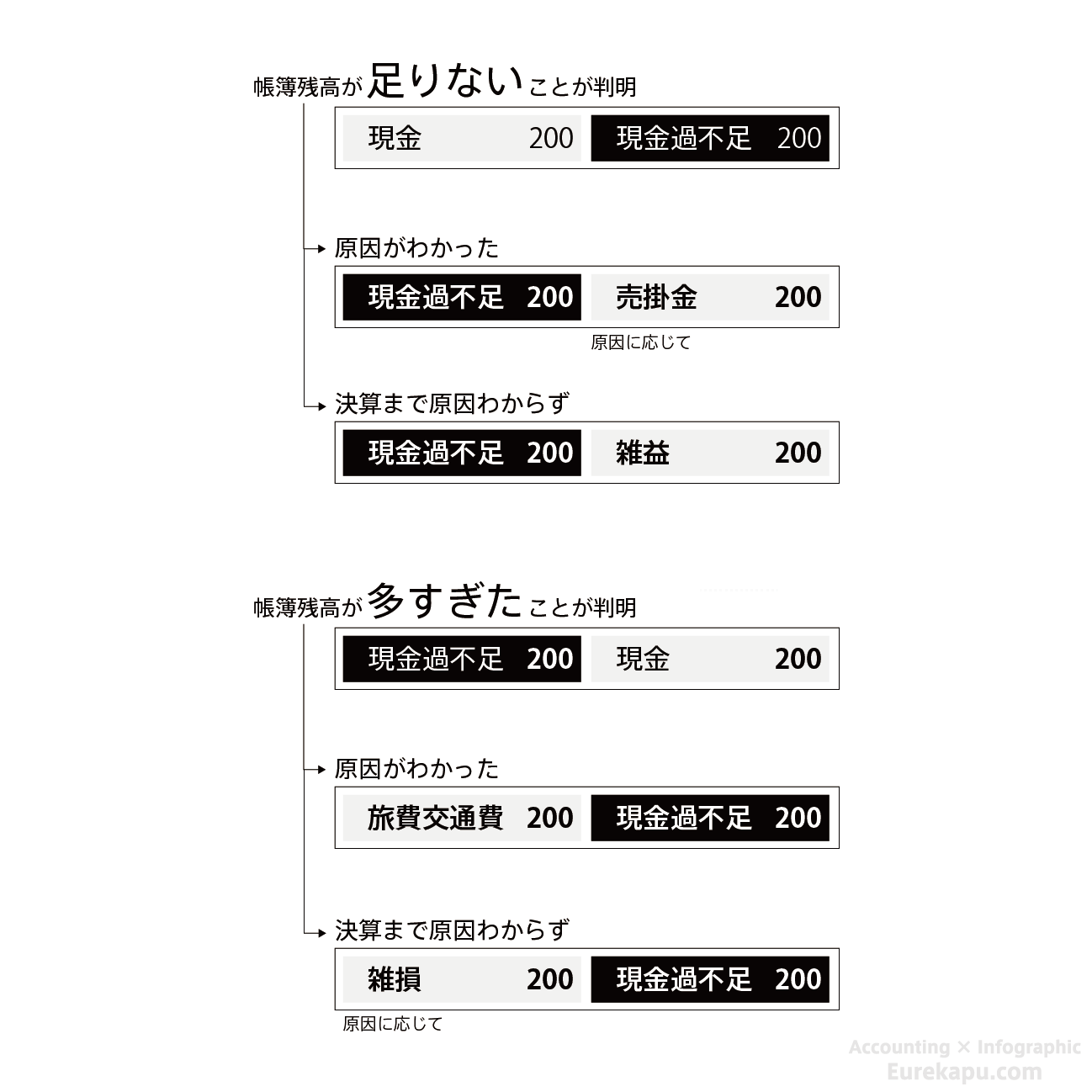

手元の現金が少ないときは借方の勘定科目に「現金過不足」を使って、仕訳をします。 反対に現金が多いときは貸方に「現金過不足」を記載します。

キャッシュ

現金過不足は費用ですか?

現金過不足という勘定科目は借方にあるときには費用になります。 厳密には費用ではありませんが、費用と考えたほうが理解しやすいので、費用と考えましょう。 20,000円現金が少ないということは、20,000円損したと考えます。 費用の発生と考えて借方に現金過不足という勘定科目を使います。

キャッシュ

現金過不足の勘定科目の借方は?

その際は、「雑損失(雑損)」、「雑収入(雑益)」の勘定科目で振替処理をします。 ケース1のように、実際の現金が少ないまま決算を迎えた場合は借方に「雑損失(雑損)」、貸方に「現金過不足」を使用し、以下のように記帳しましょう。

現金過不足は不課税ですか?

一方、②現金過不足については、資産の譲渡等の対価として処理した金額と実際の入金額との差異として生じたものであり、資産の譲渡等の対価そのものではありませんから、課税の対象となりません。

現金過不足の仮勘定とは?

現金過不足(げんきんかふそく)とは、現金出納帳の帳簿残高と実際の手許現金有高の不一致がある場合において、その不一致の原因がわからないときにその原因がわかるまでの間、これを一時的に処理するための仮の勘定科目をいう。

現金過不足は雑損処理ですか?

決算まで原因が判明しなかったときの処理

決算において現金過不足勘定に残高が残っている場合、そのすべてを雑損勘定(費用)へ振り替えます。 現金過不足勘定の金額はすべて他の勘定へ振り替えられることによって、最終的にはゼロになって消えます。

現金紛失の仕訳は?

◎現金が盗難にあった場合の経理処理

経理処理としては、盗難にあった時点で、現金過不足や仮払金(現金盗難)としておき、決算時に雑損失とする方法や、直接雑損失とする方法のいずれでも構いません。

現金過不足 どちらに合わせる?

現金過不足が出てしまい原因が分かるまでの間は、そのまま「現金過不足」という勘定科目を使って仕訳します。 重要なのは、「実際の現金残高」に合わせるように仕訳することです。

雑益勘定とは何ですか?

解説 営業外収益のうち、科目的にも金額的にも重要性が乏しいと考えられる項目を処理する勘定科目。 雑収入ともいう。

現金過不足とはどういう意味ですか?

現金過不足とは、会社で管理する現金が帳簿である現金出納帳の残高と一致しない場合の差額を指します。 小売りなど現金でのやりとりが多いほど、現金過不足は起きやすい傾向があります。 最近は自動でお釣りが出てくるレジもありますが、一般的なレジシステムで人が管理をする上では、何らかのミスは避けられません。

キャッシュカード発行料の勘定科目は?

手数料の勘定科目は「支払手数料」

例えば、クレジットカードの発行手数料・決済手数料、銀行の振込手数料、証明書の発行手数料、事務手数料(登録手数料、解約手数料など)、各種サービスの利用手数料などが挙げられます。

カード明細発行手数料の勘定科目は?

その手数料は「支払手数料」という勘定科目で記帳しましょう。

値引きは雑収入ですか?

1.リベートや値引きの処理

リべートや値引きで金銭を受け取ったときは、 「雑収入」となりますから、営業外収益として収入金額として処理します。 ただ、リベートや値引き、返品であれば、仕入金額からその分を差し引くやり方もあります。 製造業のように原価を正確に計算するというときには、このやり方がいいでしょう。

雑益と雑収入の違いは何ですか?

雑収入は「雑益」とも呼ばれており、例えば法人税や都道府県民税の還付加算金などが含まれる。 そんな雑収入を計上する規則については、以下のように定められている。 つまり、営業外収益のほかの勘定科目に当てはまらない収益であっても、一定以上の金額であれば雑収入には含まれないため注意しておきたい。

印鑑証明書は何費?

印鑑証明の取得費用は租税公課などで処理する

印鑑証明を取得する際に支払った手数料は、租税公課で処理するのが一般的です。 そのほか重要度などに合わせて、支払手数料や雑費でも処理できます。 ただし支払手数料や雑費で書類する場合は、会計ソフトの消費税の区分設定が課税仕入のままになっている可能性があるため注意しましょう。

ガソリン代の勘定科目は?

ガソリン代に使える一般的な勘定科目は車両費、旅費交通費、燃料費ですが、事業全体におけるガソリン代の金額や事業内容によっては、消耗品費や売上原価(仕入)も使えます。

駐車代は何費?

一般的に、駐車場代は、月極であれば勘定科目[地代家賃]、コインパーキングであれば勘定科目[旅費交通費]を用いて記帳します。

コピー代は何費?

コンビニでコピーを取る場合と同様に、消耗品費または雑費という勘定科目を使用するのが一般的です。 ただし、状況によっては事務用品費、仕入(売上原価)という勘定を使用することもできます。 また、貯蔵品や消耗品のような資産勘定を用いることも可能です。

キャッシュバックは何費?

法人カードを利用した際にキャッシュバックを受けた場合、「雑収入」という勘定科目を用いて会計処理することが一般的です。 一方、自社がキャッシュバックした際には、「販売促進費」や「広告宣伝費」といった勘定科目で処理します。 本記事では、キャッシュバックをされたとき・したときの仕訳を、表を用いて解説します。